A traditional bank savings account in 2026 pays roughly 0.01% to 0.5% annual interest. A high-yield savings account at the same FDIC insurance level pays 4.0% to 4.7%. The difference on a $20,000 emergency fund is approximately $850 per year of free money, just for moving the account.

Yet most Americans still keep their emergency funds in low-interest accounts at the same big bank where they have their checking. The mental friction of switching is the only thing standing between them and meaningful annual returns on idle cash.

This guide compares the best high-yield savings accounts (HYSAs) in 2026 across rates, fees, transfer speed, and bundled features. By the end, you will know exactly which account fits your situation and how to switch in under 30 minutes.

What Is a High-Yield Savings Account?

A high-yield savings account is an FDIC-insured savings account that pays significantly higher interest than traditional brick-and-mortar bank savings accounts. Most are offered by online banks (Marcus, Ally, Discover) or fintech companies (SoFi, Wealthfront, Betterment). They are functionally identical to regular savings accounts: liquid, FDIC-insured up to $250,000, and accessible through online and mobile banking.

The reason online banks pay more is structural. They have no branch overhead. They pass that cost savings to depositors as higher interest rates. The deposits are still held at FDIC-insured banks, so the safety profile is the same as any traditional bank savings account.

How We Picked the Top Accounts

Five factors matter most when evaluating an HYSA: APY (annual percentage yield), minimum balance requirements, fees, transfer speed (ACH transfer time to and from external accounts), and additional features (sub-accounts, savings goals, mobile app quality). Promotional rates that drop after a few months were excluded in favor of accounts with sustained competitive rates.

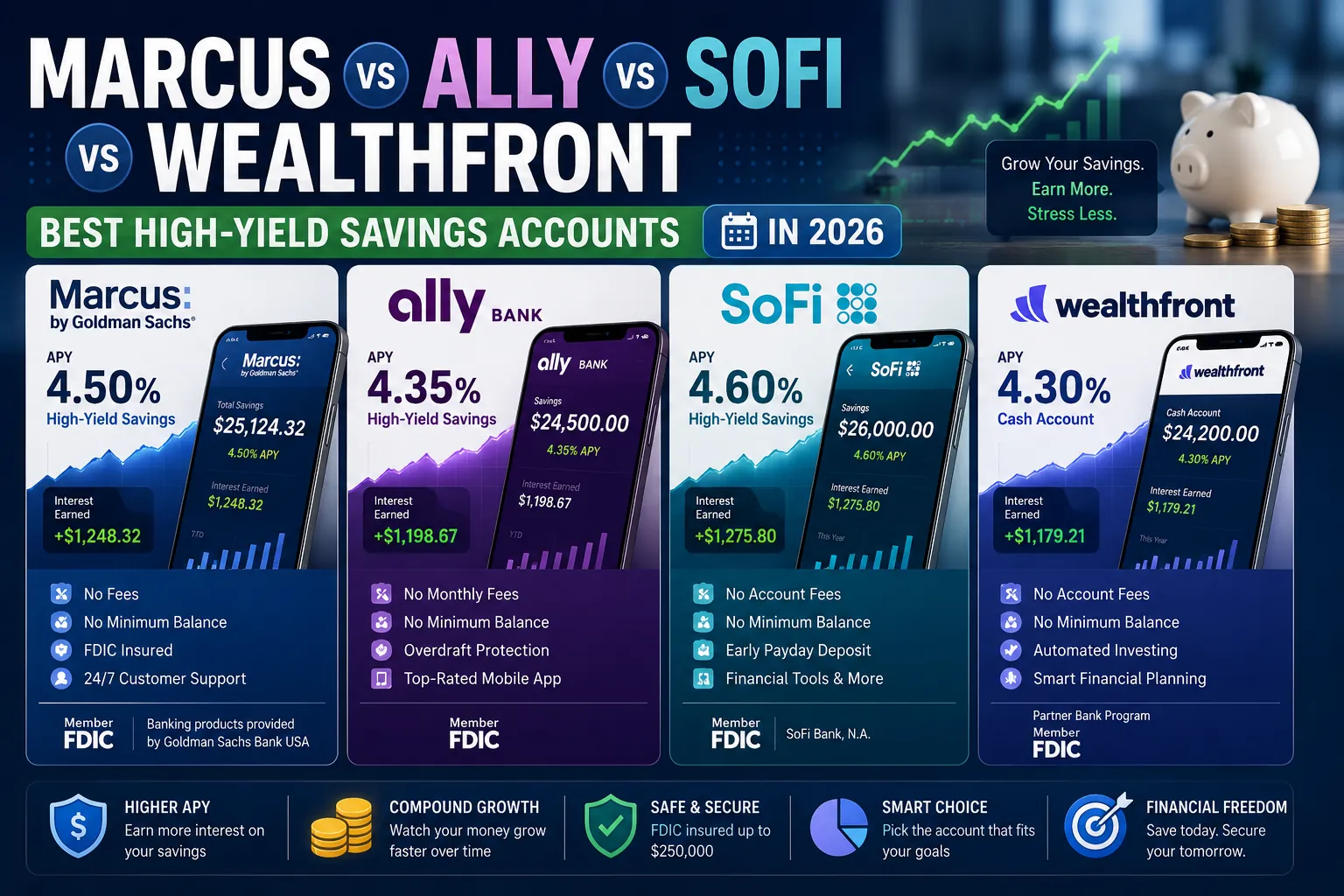

1. Marcus by Goldman Sachs

Marcus is the digital savings arm of Goldman Sachs. It has been one of the most consistent high-yield offerings since 2016, rarely chasing the absolute top of the market but rarely falling out of the top tier either. For users who value stability and a strong banking parent, Marcus is the safe default.

Strengths

- No fees, no minimum balance, no minimum to open.

- Strong customer service with US-based phone support.

- Backed by Goldman Sachs (FDIC-insured up to $250,000 per depositor).

- Same-day or next-day ACH transfers to and from external bank accounts.

Weaknesses

- No checking account or debit card option.

- Sub-account organization is limited compared to Ally or SoFi.

- APY is competitive but rarely the absolute highest.

Current APY (April 2026)

Approximately 4.20% to 4.40% APY. Always check the live rate before opening.

2. Ally Bank Online Savings

Ally is the longest-running fully online bank in the US (since 2009) and remains a category benchmark for HYSAs. Its sub-account “buckets” feature allows you to organize savings goals visually within a single account, which has become a standard feature competitors have copied.

Strengths

- No fees, no minimum balance.

- Buckets feature lets you create up to 30 sub-savings goals within one account.

- Surprise Savings (automated savings boosts based on checking activity).

- Free ATM access at Allpoint network plus rebates for out-of-network ATMs.

- Strong companion checking account if you want to consolidate banking.

Weaknesses

- APY can lag the top fintech HYSAs by 0.10% to 0.30%.

- Mobile app, while solid, is not as polished as SoFi or Wealthfront.

Current APY (April 2026)

Approximately 4.00% to 4.20% APY.

3. SoFi Money / SoFi Savings

SoFi has built a full digital banking experience around its HYSA, including checking, investing, lending, and budgeting. The combined account view is the most modern banking experience available in 2026, and the HYSA rate is consistently among the highest mainstream options.

Strengths

- Among the highest mainstream HYSA rates in 2026.

- Bundled checking with no fees, plus debit card with strong cashback.

- Full ecosystem: investing, loans, credit cards, all in one app.

- FDIC insurance up to $2 million through partner bank network (above the standard $250,000).

Weaknesses

- Higher rate often requires direct deposit setup (otherwise drops to standard tier).

- Strong push to upsell investing and lending products.

- Some features change frequently as SoFi iterates on its product.

Current APY (April 2026)

Approximately 4.50% to 4.70% APY with direct deposit. Around 1.20% APY without.

4. Wealthfront Cash Account

Wealthfront started as a robo-advisor and added a cash account in 2019. It has become one of the most competitive HYSAs in 2026, with extended FDIC insurance through partner banks and seamless integration with Wealthfront’s investment products.

Strengths

- Consistently top-tier APY without rate-tiering tricks.

- FDIC insurance up to $8 million through 32 partner banks.

- Same-day transfers to Wealthfront investment accounts.

- No fees, no minimum balance after a $1 opening deposit.

- Direct deposit available with debit card.

Weaknesses

- No physical branch network or check-writing capability.

- Best value comes from also using Wealthfront for investing.

Current APY (April 2026)

Approximately 4.50% to 4.75% APY (with referrals adding +0.50% for 3 months).

Honorable Mentions

- Discover Online Savings: consistently competitive APY, no fees, strong customer service. Slightly less feature-rich than Ally but reliable.

- Capital One 360 Performance Savings: best for users who already bank with Capital One and want sub-savings buckets.

- CIT Bank Platinum Savings: higher APY for balances above $5,000, lower for smaller balances. Good for larger emergency funds.

- Betterment Cash Reserve: similar to Wealthfront with extended FDIC insurance, slightly lower APY.

Side-by-Side Comparison

| Account | Approx APY | Min Balance | Standout Feature | Best For |

|---|---|---|---|---|

| Marcus | 4.20% to 4.40% | $0 | Goldman Sachs reliability | Conservative savers |

| Ally | 4.00% to 4.20% | $0 | Buckets sub-savings goals | Goal-based savers |

| SoFi Savings | 4.50% to 4.70% | $0 | Full banking ecosystem | Younger, app-first users |

| Wealthfront Cash | 4.50% to 4.75% | $1 | $8M FDIC coverage | Larger balances, investors |

| Discover Savings | 4.10% to 4.30% | $0 | Strong customer service | Traditional bank refugees |

| CIT Platinum | 4.50% to 4.85% | $5,000 | Highest tier rate above $5k | Larger emergency funds |

How to Switch From a Traditional Bank to an HYSA

Switching is faster and easier than most people expect. The complete process:

- Pick one HYSA from the list above based on your priorities (rate, ecosystem, FDIC coverage).

- Open the new account online. Most take 5 to 10 minutes and require basic personal info plus your existing bank account details for funding.

- Initiate an ACH transfer from your old savings account to the new HYSA. Transfers take 1 to 3 business days.

- Update direct deposit, automatic transfers, and any recurring funding rules to point to the new account.

- Once the new account is funded and all automation is updated, leave the old account open with $0 balance for at least 60 days in case of any pending transactions.

- Close the old account after 60 to 90 days if you have no need to keep it open.

When an HYSA Is Not the Right Tool

High-yield savings accounts are excellent for emergency funds, short-term savings goals, and idle cash you may need within a few years. They are not the right tool for:

- Long-term retirement savings. A 401(k), IRA, or taxable brokerage account in low-cost index funds will dramatically outperform any HYSA over decades.

- Money you need in the next 30 days. Use checking or money market accounts for liquidity within the month. ACH transfers can take 1 to 3 days.

- Goals that need lower volatility than stocks but higher returns than savings. I-Bonds, Treasury bills, and short-term bond ETFs may serve better for 1 to 5 year goals.

Common HYSA Mistakes

- Chasing rates monthly. Switching banks every time another offers 0.05% more is not worth the friction. Pick a top-tier account and stay unless rates diverge significantly.

- Ignoring the fine print on tiered rates. Some accounts pay higher rates only on certain balance ranges or with direct deposit conditions. Read the rate disclosure.

- Keeping more than $250,000 in a single bank without spreading. FDIC insurance covers $250,000 per depositor per bank. Beyond that, use multiple banks or services with extended coverage (Wealthfront, SoFi).

- Forgetting that interest is taxable. HYSA interest is taxed as ordinary income. Set aside 22% to 32% of your interest for federal taxes plus state if applicable.

Expert Tips

- Set up automatic transfers from checking. Even small automatic deposits ($25 to $100 weekly) build emergency savings without willpower.

- Use the buckets or sub-account feature. Visualizing distinct savings goals (vacation, taxes, emergency) inside one account improves discipline.

- Re-evaluate annually. Top HYSA rates shift over time as Fed rates change. A quick yearly review keeps your money in a top-tier account.

- Open the new account before fully closing the old one. Brief overlap prevents friction with autopay rules and pending transactions.

Frequently Asked Questions

Are high-yield savings accounts safe?

Yes. The HYSAs in this guide are FDIC-insured up to at least $250,000 per depositor. Several (Wealthfront, SoFi, Betterment) extend coverage to $2 to $8 million through partner bank networks. The safety profile is identical to a traditional bank savings account at any FDIC-insured institution.

How often do HYSA rates change?

HYSA rates generally track the Federal Reserve’s federal funds rate. When the Fed raises rates, HYSAs typically increase within 30 to 60 days. When the Fed cuts rates, HYSAs decrease at a similar pace. Specific rate changes can happen weekly at fintech HYSAs and quarterly at established online banks.

Should I keep my emergency fund in a single HYSA or spread it across several?

For emergency funds under $250,000, a single HYSA is fine because that amount is fully covered by FDIC insurance. For larger balances, spread across two or three institutions or use accounts with extended FDIC coverage like Wealthfront ($8M coverage) or SoFi ($2M coverage). The peace of mind is worth the small organizational effort.

Can I lose money in a high-yield savings account?

No, in the same way you cannot lose money at a traditional bank savings account. HYSAs are FDIC-insured deposit accounts, not investments. The principal is protected. The interest rate can change, but you cannot lose your deposit balance. Inflation can reduce purchasing power over time, which is why HYSAs are intended for emergency funds and short-term savings rather than long-term wealth building.

The Easiest Money You Will Make This Year

Switching to a high-yield savings account is the closest thing to free money in personal finance. The process takes 30 minutes. The annual return is hundreds to thousands of dollars depending on your balance. The risk is the same as any FDIC-insured savings account.

Pick one of the top accounts from this guide, open it this week, and move your idle cash. Then leave it alone and let the compounding work.

For the complete personal finance roadmap covering budgeting, debt, investing, and the foundational pillars of financial life, read our pillar: Personal Finance in 2026: A Complete Guide. More money guides live on PostoryCafe.com.