Personal finance in 2026 is more accessible, more automated, and more confusing than at any previous point in history. Banking apps track every dollar. Investment platforms let you buy fractional shares of any company with a tap. AI advisors generate personalized financial plans in seconds. And yet, more than 60% of Americans live paycheck to paycheck, and household debt has reached record highs.

The tools have multiplied. The behaviors that drive financial outcomes have not. Spending less than you earn, building an emergency fund, paying down high-interest debt, and investing consistently for the long term are still the foundations. The technology of 2026 makes these easier to execute than ever, if you know which tools to use and which advice to ignore.

This guide covers the complete personal finance picture in 2026: the budgeting frameworks that actually work, how to build emergency savings, smart debt management, investing for beginners, and the tools that make all of it easier. It is built for people who want a clear roadmap rather than another reminder that they should “spend less.”

The State of Personal Finance in 2026

Three forces shape personal finance today. First, inflation has cooled from the 2022 peak but accumulated significantly: prices in 2026 are roughly 25% higher than in 2020 across food, housing, healthcare, and education. Second, real wages have grown but unevenly, with significant variation by industry and geography. Third, the financial tools available to consumers have improved dramatically, with AI-driven advisors, automated savings, and zero-fee investing now standard.

For the average person, this means the rules of good financial behavior are unchanged but the cost of bad behavior is higher. A poorly managed credit card balance compounds at 22 to 28% APR. A missed retirement contribution loses decades of growth. The penalty for financial inattention has grown.

The 4 Foundational Pillars of Personal Finance

Personal finance has gotten complicated, but the foundations remain simple. Master these four, in order, and your financial life works.

| Pillar | Goal | Why It Comes First |

|---|---|---|

| 1. Budget | Spend less than you earn | Without this, nothing else matters |

| 2. Emergency Fund | Cover 3 to 6 months of expenses | Prevents debt during life surprises |

| 3. Debt Management | Eliminate high-interest debt | 22%+ credit card APR beats most investment returns |

| 4. Investing | Build long-term wealth | Compound growth requires time, start as soon as possible |

Pillar 1: Budgeting Frameworks That Work in 2026

A budget is not a punishment. It is permission to spend on what actually matters by being conscious about what does not. The right framework depends on your personality and how much active management you want to do.

The 50/30/20 Rule

50% of your post-tax income goes to needs (rent, groceries, transportation, insurance, minimum debt payments). 30% goes to wants (dining out, entertainment, hobbies, vacations). 20% goes to savings and additional debt repayment beyond minimums.

For most people earning a stable salary, 50/30/20 is the most balanced framework. It avoids the deprivation of too-strict budgets and the lack of structure of pure tracking. In high cost of living areas, the split often becomes 60/20/20 or 65/15/20, which is fine as long as savings stay at 15% or higher.

Zero-Based Budgeting

Every dollar of income gets assigned a job before the month begins. If you earn $5,000, you allocate every dollar (rent, groceries, savings, debt payment, entertainment, etc.) until the budget reaches zero. Apps like YNAB (You Need a Budget) build entire workflows around this method.

Zero-based budgeting works exceptionally well for people with variable income, those getting out of debt, or anyone who struggles with overspending. It requires more active management than 50/30/20.

The Pay Yourself First Approach

Automate savings and investments to come out of your paycheck before you ever see the money. Whatever is left covers everything else. This works because it forces savings to happen automatically rather than depending on what is “left over” at month end (which often is not much).

For high earners with predictable income, pay-yourself-first is often the most sustainable approach. It eliminates the willpower battle and reduces the need for active expense tracking.

Pillar 2: Building an Emergency Fund

An emergency fund is the cash buffer that protects you from going into debt when life surprises happen: medical bills, car repairs, job loss, family emergencies. Without it, every minor crisis becomes a credit card balance that compounds at high interest.

The standard recommendation: 3 to 6 months of essential expenses in a high-yield savings account. For someone with stable employment, 3 months is usually sufficient. For freelancers, single-income families, or those in volatile industries, 6 to 9 months is more appropriate.

Where to Keep Your Emergency Fund

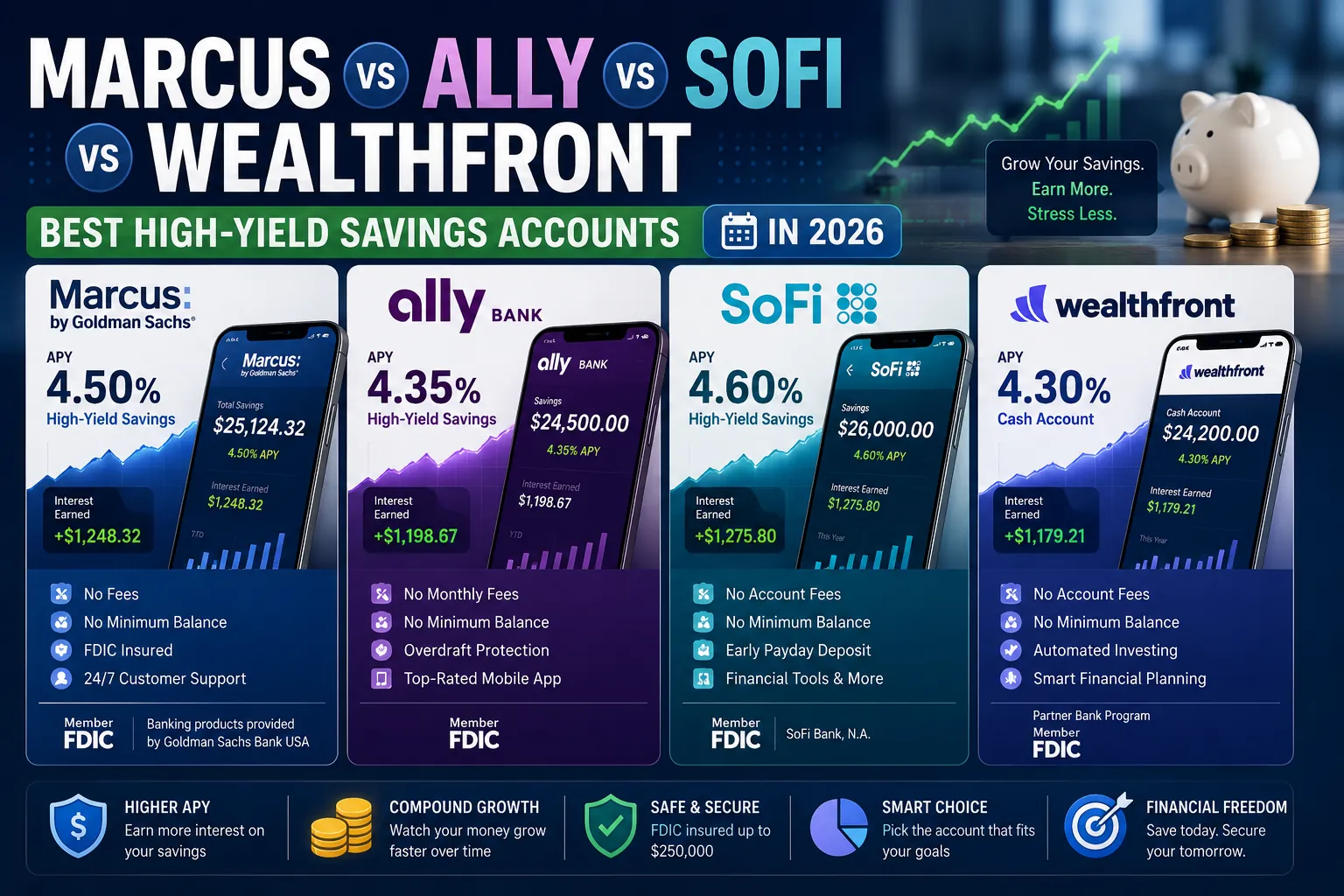

High-yield savings accounts (HYSAs) at online banks are the right home. In 2026, HYSAs at Marcus, Ally, Discover, SoFi, and Wealthfront pay 4.0% to 4.7% APY, dramatically more than traditional bank savings accounts. The money stays liquid (accessible within 1 to 2 business days) while still earning real returns.

Avoid keeping the emergency fund invested in stocks. Investments swing 20 to 40% in normal market cycles. The whole point of an emergency fund is having it available when you need it without having to sell at a loss.

Pillar 3: Smart Debt Management

Not all debt is the same. Mortgage debt at 6.5% looks different from credit card debt at 24%. The right debt strategy depends on what kind of debt you have and at what interest rate.

High-Interest Debt: Eliminate Aggressively

Any debt above 8% APR (most credit cards, high-rate personal loans, payday loans) should be paid down before significant investing. The math is simple: the guaranteed return from eliminating 22% APR debt beats the historical 7% real return of stock market investments.

Two methods work for paying down multiple debts:

- Avalanche method: pay minimums on all debts, then apply every extra dollar to the highest-interest debt first. Mathematically optimal.

- Snowball method: pay minimums on all debts, then apply every extra dollar to the smallest balance first. Less mathematically optimal but more psychologically motivating because of the quick win of eliminating individual debts.

Both work. Pick the one you will stick with.

Lower-Interest Debt: Invest in Parallel

Mortgage debt at fixed rates below 6%, federal student loans at 4 to 6%, and similar lower-rate debts can be paid on schedule while you also invest. The expected return from long-term stock investing exceeds the cost of these debts. Refinancing high-rate debt to lower rates (when possible) compounds the benefit.

Pillar 4: Investing for Long-Term Wealth

Investing is how money grows beyond what saving alone can produce. Saving $500 per month for 30 years at zero return produces $180,000. Investing the same amount at the historical 7% real return of US stocks produces over $613,000. Compound growth, given enough time, dwarfs principal contributions.

The Investing Hierarchy

Most personal finance experts agree on the right order to invest dollars in 2026.

- 1. Capture employer 401(k) match. This is free money. If your employer matches 5% of contributions, contribute at least 5%. Failing to do so is leaving compensation on the table.

- 2. Pay off high-interest debt aggressively. Above 8% APR, debt elimination beats most investment returns.

- 3. Max out an HSA if eligible. Health Savings Accounts offer triple tax advantages and become a powerful retirement vehicle for people on high-deductible health plans.

- 4. Max out IRA contributions. Roth IRA for tax-free growth if you qualify. Traditional IRA for tax-deferred growth otherwise. The 2026 contribution limit is $7,500 ($8,500 if over 50).

- 5. Continue 401(k) contributions to the annual max. $24,000 in 2026 ($31,500 if over 50).

- 6. Invest in a taxable brokerage account. No contribution limits. Diversified low-cost index funds (Vanguard VTSAX, FZROX, SCHB) are the standard recommendation.

- 7. Consider real estate, individual stocks, or alternative investments. Only after the foundations above are well-established.

The Three-Fund Portfolio

For new investors, a simple three-fund portfolio captures global stock and bond exposure at minimum cost: a US total stock market index fund (VTSAX, FZROX), an international stock index fund (VTIAX, FTIHX), and a total bond fund (VBTLX, FXNAX). A typical allocation might be 60% US stocks, 30% international stocks, 10% bonds, adjusted for age and risk tolerance.

This three-fund approach has consistently outperformed actively managed funds over long periods because of lower expense ratios. Vanguard, Fidelity, and Schwab all offer these funds with expense ratios near zero.

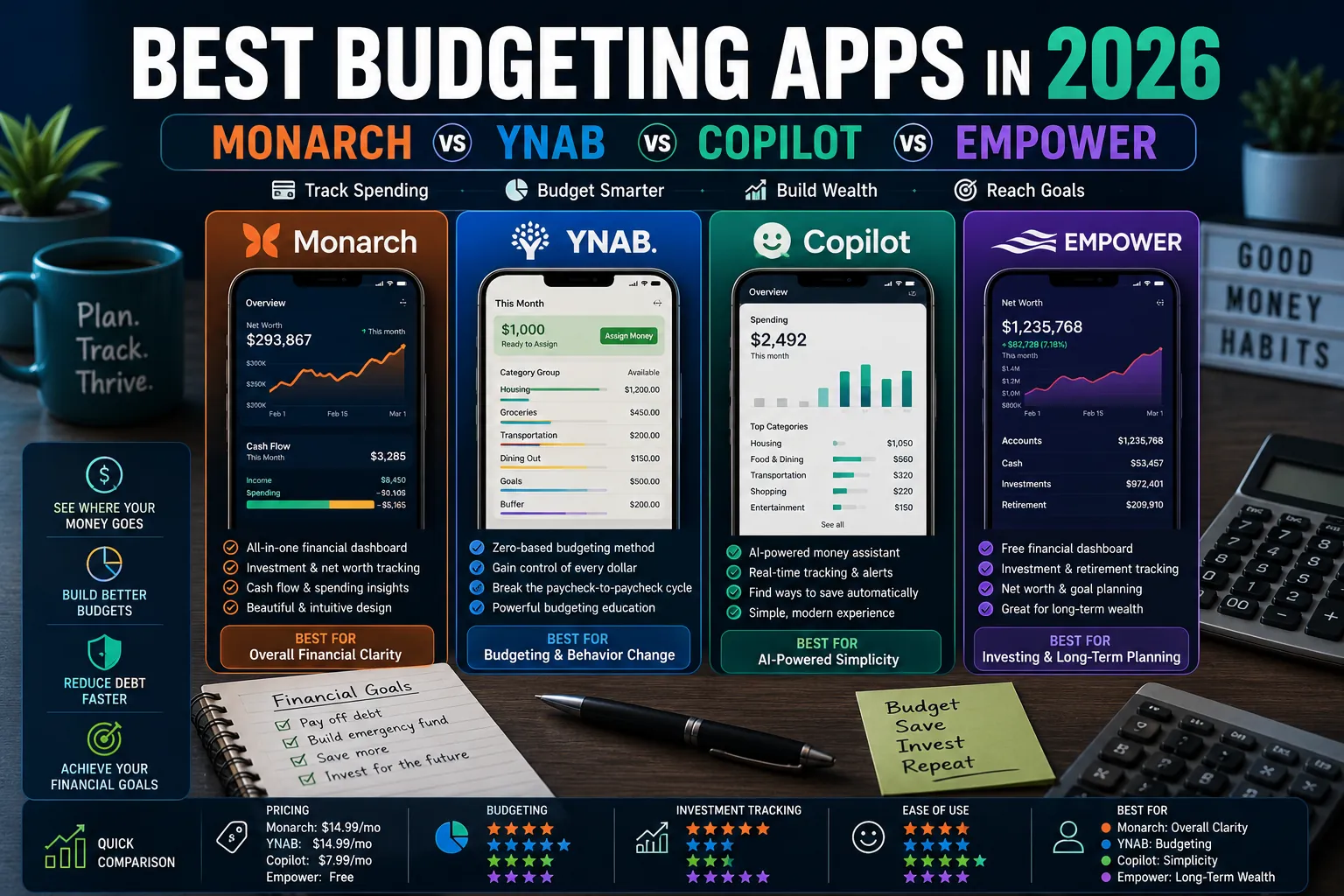

The Best Personal Finance Apps in 2026

| App | Best For | Cost |

|---|---|---|

| Monarch Money | Budgeting and net worth tracking | $15/month or $100/year |

| YNAB (You Need a Budget) | Zero-based budgeting and behavior change | $15/month or $109/year |

| Copilot Money | Premium iOS budgeting experience | $13/month or $95/year |

| Empower (formerly Personal Capital) | Investment tracking and net worth | Free with paid advisor option |

| Wealthfront / Betterment | Automated investing (robo-advisor) | 0.25% AUM annual fee |

| Fidelity, Vanguard, Schwab | DIY brokerage with index funds | Free trades, low expense ratios |

| Marcus, Ally, SoFi | High-yield savings accounts | Free, 4.0%+ APY |

7 Common Personal Finance Mistakes

- Skipping the emergency fund. Investing before having 3 months of expenses saved means a single emergency derails your entire plan with high-interest debt.

- Trying to beat the market with active stock picking. Index fund investing has consistently outperformed active management over 10-year+ periods. The data is overwhelming.

- Lifestyle inflation. When income rises, expenses rise to match. The result: higher earners with no more savings than they had before. Direct raises and bonuses to savings before they enter your spending pattern.

- Ignoring tax-advantaged accounts. Maxing 401(k) match and Roth IRA before taxable investing is one of the highest-value financial decisions available. Many people skip it because the rules feel complicated.

- Carrying credit card debt while investing. Investing with a 22% APR credit card balance is mathematically guaranteed to lose money. Eliminate the debt first.

- Following financial advice from social media without verification. TikTok and Instagram have dramatically increased the volume of financial misinformation reaching consumers. Verify any specific advice through reputable sources before acting.

- Treating insurance as optional. Health insurance, auto insurance, renter’s or homeowner’s insurance, and term life insurance for those with dependents are not optional. Going without is gambling against catastrophic loss.

Expert Tips

- Automate everything possible. Direct deposit splits, automatic bill pay, automatic 401(k) contributions, and automatic transfers to savings remove willpower from the equation. The most successful financial behaviors run without active management.

- Calculate your savings rate. Total saved divided by total income. A 15% savings rate is the minimum for a middle-class retirement. 25%+ creates real wealth and optionality.

- Track net worth quarterly, not weekly. Daily portfolio checking creates anxiety without information value. Quarterly reviews show real progress.

- Read one good personal finance book. “The Simple Path to Wealth” by JL Collins, “I Will Teach You to Be Rich” by Ramit Sethi, or “The Psychology of Money” by Morgan Housel are the most-recommended starting points in 2026.

- Get a fee-only financial planner for major decisions. A few hundred dollars for an hour with a fiduciary CFP is worth dramatically more than an asset-managed advisor for major decisions like home buying, retirement planning, or estate planning.

Frequently Asked Questions

How much should I save each month?

A widely accepted target is 15% to 20% of pre-tax income across retirement contributions, emergency fund, and other savings combined. Higher savers (25% or more) build significant wealth and optionality. The right number depends on your goals, age, and current financial position. Someone starting late may need to save 25% or more to catch up. Someone starting at 22 can build substantial wealth with 15%.

What is the best way to start investing?

For beginners in 2026, the simplest and most evidence-backed approach is contributing to your employer 401(k) up to the match, opening a Roth IRA at Vanguard or Fidelity, and investing in low-cost target-date funds or a simple three-fund portfolio. This approach captures global market returns at minimum cost without requiring stock-picking skill or active management. Robo-advisors like Wealthfront and Betterment offer similar exposure with slightly higher fees but more hand-holding.

Should I pay off debt or invest first?

High-interest debt (above 8% APR) should be paid off before substantial investing because the guaranteed return from elimination beats expected investment returns. The exception is your employer 401(k) match, which is free money and should be captured even while paying down debt. Lower-rate debt (mortgages, federal student loans below 6%) can be paid on schedule alongside investing.

What is a high-yield savings account and why does it matter?

A high-yield savings account (HYSA) is an FDIC-insured savings account at an online bank that pays significantly more interest than traditional brick-and-mortar bank savings accounts. In 2026, HYSAs typically pay 4.0% to 4.7% APY versus 0.01% to 0.5% at most large traditional banks. The difference on a $20,000 emergency fund is approximately $850 per year. Switching is free and takes 15 minutes.

How much should I keep in an emergency fund?

The standard recommendation is 3 to 6 months of essential expenses in a high-yield savings account. For someone with stable W-2 employment, 3 months is typically sufficient. For freelancers, single-income families, contractors, or those in volatile industries, 6 to 9 months provides better protection. Beyond 9 months in cash is generally not optimal because additional savings are better deployed in retirement or investment accounts.

Are robo-advisors better than financial advisors?

For most people with under $500,000 in investable assets, robo-advisors like Wealthfront and Betterment provide the same core service (diversified portfolios, automatic rebalancing, tax-loss harvesting) at one-tenth the cost of human advisors. Human advisors add value for complex situations: estate planning, business sales, tax strategy, behavioral coaching during volatile markets. For straightforward investment management, robo-advisors win on cost.

Build the Financial Life That Fits You

Personal finance in 2026 has more tools than any previous era and the same underlying mathematics. Spend less than you earn. Build an emergency fund. Eliminate high-interest debt. Invest consistently in low-cost diversified funds. Automate everything possible. Read one good book. Talk to a fee-only financial planner before major decisions.

The discipline is harder than the knowledge. The technology of 2026 makes the discipline easier than ever, by automating savings, eliminating fees, and making investing accessible to anyone with a smartphone. The opportunity to build real long-term wealth is still there. It just requires showing up consistently for the next 20 to 40 years.

For more practical guides on budgeting, investing, debt reduction, and financial independence, explore the Personal Finance category on PostoryCafe.com. We publish new content every week to help readers build the financial life that fits their goals and stage of life.